EPSS information

Explanations:

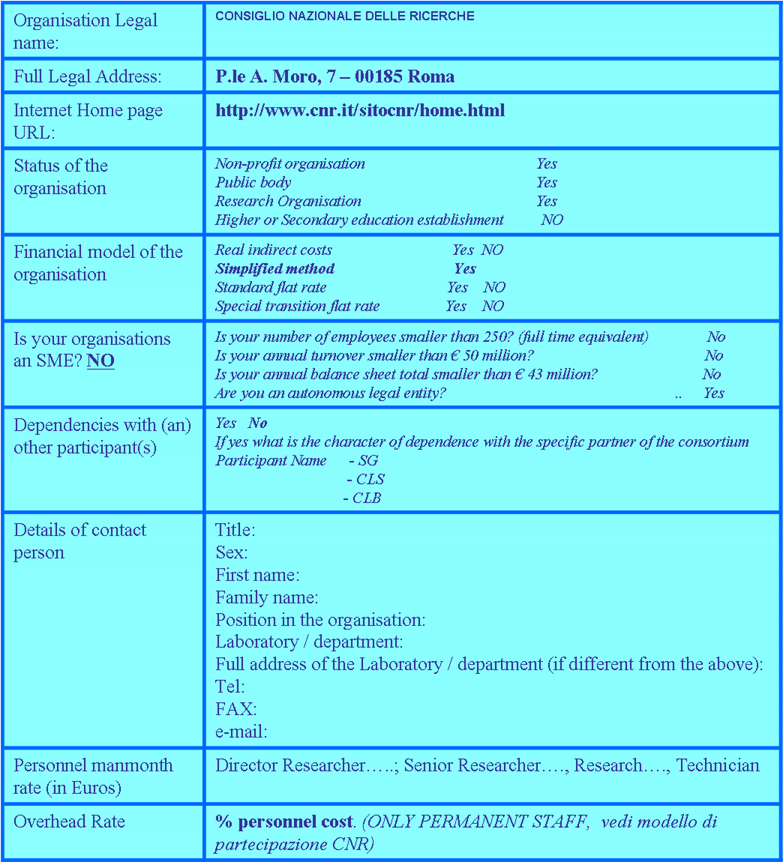

Legal name For Public Law Body, it is the name under which your organisation is registered in the Resolution text, Law, Decree/Decision establishing the Public Entity, or in any other document established at the constitution of the Public Law Body;

For Private Law Body, it is the name under which your organisation is registered in the national Official Journal (or equivalent) or in the national company register.

For a natural person, it is for e.g. Mr Adam JOHNSON, Mrs Anna KUZARA, and Ms Alicia DUPONT.

Legal address: For Public and Private Law Bodies, it is the address of the entity’s Head Office. For Natural persons it is the Official Address. If your address is specified by an indicator of location other than a street name and number, please insert this instead under the "street name" field and "N/A" under the "number" field.

Non-profit organisation: Non-profit organisation is a legal entity qualified as such when it is recognised by national or, international law.

Public body: Public body means any legal entity established as such by national law, and international organisations.

Research organisation: Research organisation means a legal entity established as a non-profit organisation which carries out research or technological development as one of its main objectives.

Financial Models in 7FP

The models for the 7FP are the following

- Real indirect costs: Real indirect costs incurred in direct relationship with the direct eligible costs attributed to the action calculated using an analytical accounting system

- Simplified method: A participant may use a simplified method of calculation of its full indirect eligible cost at the level of its legal entity if it is in accordance with its usual accounting and management principles and practices. Use of such a method is only acceptable where the lack of analytical accounting or the legal requirement to use a form of cash-based accounting prevents detailed cost allocation. The simplified approach must be based on actual costs derived from the financial accounts of the period in question.

- Standard flat rate: A participant may opt for a flat-rate of 20% of its total direct eligible costs, excluding its direct eligible costs for subcontracting and the costs of reimbursement of resources made available by third parties which are not used on the premises of the participant.

- Special transition flat rate: Non-profit public bodies, secondary and higher education establishments, and research organisations and SMEs, which are unable to identify with certainty their real indirect costs for the project, when participating in funding schemes which include research and technological development and demonstration activities may opt for a flat-rate of 60% of the total direct eligible costs1 excluding costs for subcontracting and the costs of reimbursement of resources made available by third parties which are not used on the premises of the participant. If these participants change their status during the life of the project, this flat rate shall be applicable up to the moment they lose their status.

Small and Medium Sized: SMEs are micro, small and mediumsized enterprises within the meaning of Recommendation 2003/361/EC in the version of 6 May 2003. The full definition and a guidance booklet can be found at: http://ec.europa.eu/enterprise/enterprise_policy/sme_definition/index_en.htm

Dependencies with (an) other participant(s): Two participants (legal entities) are dependent on each other where there is a controlling relationship between them:

- A legal entity is under the same direct or indirect control as another legal entity (SG);

- A legal entity directly or indirectly controls another legal entity (CLS);

- A legal entity is directly or indirectly controlled by another legal entity (CLB).

Control:

Legal entity A controls legal entity B if:

- A, directly or indirectly, holds more than 50% of the nominal value of the issued share capital or a majority of the voting rights of the shareholders or associates of B,

or

- A, directly or indirectly, holds in fact or in law the decisionmaking powers in B.

The following relationships between legal entities shall not in themselves be deemed to constitute controlling relationships:

(a) the same public investment corporation, institutional investor or venture capital company has a direct

(b) or indirect holding of more than 50 % of the nominal value of the issued share capital or a majority of voting rights of the shareholders or associates;

(c) the legal entities concerned are owned or supervised by the same public body.

Character of dependence: According to the explanation above mentioned, please insert the appropriate abbreviation according to the list below to characterise the relation between your organisation and the other participant(s) you are related with:

- SG: Same group: if your organisation and the other participant are controlled by the same third party;

- CLS: Controls: if your organisation controls the other participant;

- CLB: Controlled by: if your organisation is controlled by the other participant.

Contact point: It is the main scientist or team leader in charge of the proposal for the participant. For participant number 1 (the coordinator), this will be the person the Commission will contact concerning this proposal (e.g. for additional information, invitation to hearings, sending of evaluation results, convocation to negotiations).

Title: Please choose one of the following: Prof., Dr., Mr., Mrs, Ms.

Sex: This information is required for statistical and mailing purposes. Indicate F or M as appropriate.

Phone and fax numbers: Please insert the full numbers including country and city/area code. Example +3222991111.

Personnel man-month rate (in Euros): The cost for the personnel man-month

Overhead Rate: Based on the above assumptions regarding the financial model of your participation, your indirect cost rate.

Scarica il file in formato pdf